SECTION 1

You Are Not Alone — and You Are Not Failing

It is 11:47 p.m. The house is quiet. You open your banking app, again, and feel your stomach drop, again. You moved the minimum payment on the credit card last week. You will again this week. The balance barely budged. In fact, you think it might be slightly higher. You are working. You are trying. You are not buying luxuries. And yet the numbers refuse to move in your direction.

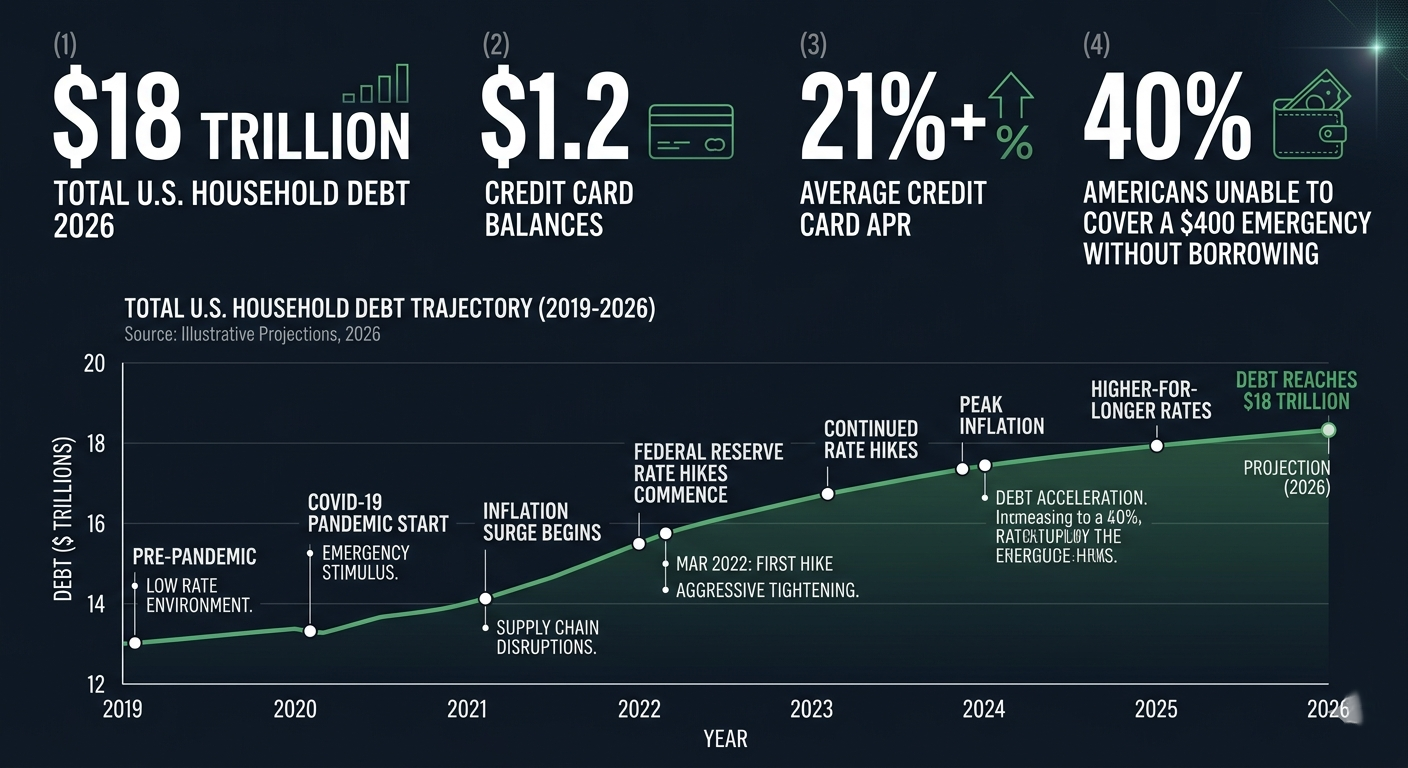

If this feels familiar, you are not alone, and you are not failing. You are navigating one of the most financially hostile environments for ordinary households in modern American history. Household debt in the United States has surpassed $18 trillion. Credit card balances have broken through $1.2 trillion for the first time. The average credit card interest rate now exceeds 21%, a figure that would have seemed shocking just a decade ago. And wages have not kept pace with the cost of everything that matters: housing, groceries, healthcare, childcare, utilities.

"The math of modern debt is not a personal failure. It is a structural reality. But within that reality, there are proven strategies — and real people have climbed out of far deeper holes than the one you are in."

This guide does not traffic in shame or false promises. It does not tell you to stop buying coffee. It will not tell you that financial peace is three easy steps away. What it will give you is an honest, practical, psychologically grounded 2026 debt payoff blueprint, one that takes seriously both the numbers and the human being behind them.

The 7 strategies in this article are time-tested, financially sound, and adaptable to a wide range of income levels and debt profiles. Some people will use one. Others will combine several. What matters is not choosing perfectly, it is choosing something, starting, and adjusting as you go. The momentum of small consistent progress is one of the most powerful forces in personal finance. Let this be where yours begins.

SECTION 2

Why Household Debt Has Exploded in 2026

To address debt effectively, it helps to understand why it has grown so dramatically, not to excuse it, but to contextualize it. Individual financial choices exist within structural economic conditions. Understanding both empowers better decision-making.

The Confluence of Pressures

Economic Force | How It Is Driving Household Debt in 2026 |

| Persistent Inflation | While headline inflation has moderated since its 2022 peaks, cumulative price increases have permanently elevated the cost of essentials. Groceries, utilities, insurance, and housing cost 20–35% more than they did in 2019, and wages have not fully compensated. |

| High Interest Rate Environment | The Federal Reserve's aggressive rate-hiking cycle pushed credit card APRs above 21% on average, with many cards charging 24–29.99%. Every dollar of unpaid balance is now dramatically more expensive to carry than at any point in the past two decades. |

| Housing Cost Crisis | Rents in major metropolitan areas have increased 40–60% since 2019. The housing cost burden is pushing more of every household's income toward shelter, leaving less for essentials and pushing other costs onto credit. |

| Wage Stagnation (in Real Terms) | While nominal wages have increased, real wage growth has been eroded by inflation. Many households are earning more dollars but buying less — creating a silent affordability squeeze that shows up as rising credit card balances. |

| Buy Now Pay Later (BNPL) Proliferation | The rapid expansion of BNPL services has normalized splitting everyday purchases into installment payments, creating a new category of consumer debt that is often invisible in standard credit reports and poorly understood by users. |

| Emergency Expenses Without Savings | A 2025 Federal Reserve survey found that more than 40% of Americans could not cover an unexpected $400 expense without borrowing. Medical bills, car repairs, and home emergencies consistently push households onto high-interest credit. |

| Pandemic Financial Scars | Millions of households depleted savings, took on debt, or used retirement funds during the pandemic years. The rebuilding of those buffers is incomplete, leaving families more financially fragile going into 2026. |

| Financial Literacy Gaps | Despite widespread smartphone access to financial tools, fundamental financial literacy, particularly around compound interest, credit utilization, and the long-term cost of minimum payments, remains low. Debt grows fastest where understanding is weakest. |

SECTION 3

The Psychological Impact of Debt

Debt is not just a financial problem. Research in behavioral economics and clinical psychology consistently shows that financial stress activates the same neural pathways as physical threat, triggering chronic stress responses that affect sleep, cognition, relationships, and physical health. Understanding the psychological dimensions of debt is not an indulgence. It is essential to effective debt management.

Psychological Impact | How It Manifests and Why It Matters |

|---|---|

| Financial Anxiety | Persistent background worry about money, often intrusive and uncontrollable. Studies link chronic financial stress to elevated cortisol, reduced working memory, and impaired decision-making. Anxiety can actually prevent the clear financial thinking needed to solve the problem. |

| Shame and Self-Blame | The cultural narrative that debt is a moral failing leads many people to internalize financial struggle as personal inadequacy. Shame is one of the primary drivers of financial avoidance, making people less likely to open statements, seek help, or engage with their finances. |

| Avoidance Behavior | When financial anxiety or shame becomes overwhelming, avoidance is a natural psychological response. Not opening bank statements, ignoring calls from creditors, and refusing to look at balances are common, and while temporarily relieving, they allow debt to compound in silence. |

| Sleep Disruption | Financial worry is among the most common reported causes of sleep disruption in adults. Poor sleep impairs emotional regulation, decision-making, and impulse control, creating a vicious cycle where financial stress worsens the cognitive capacity needed to address it. |

| Relationship Stress | Money is consistently ranked as the leading cause of relationship conflict. Debt creates divergent priorities, blame cycles, and communication breakdowns in partnerships, adding relational pressure to an already heavy burden. |

| Depression and Burnout | Chronic financial stress is independently associated with depression, emotional burnout, and reduced life satisfaction. The feeling of running hard and getting nowhere economically creates a particular kind of hopelessness that deserves both financial and emotional attention. |

| Shame-Spending Cycles | For some people, financial stress triggers emotional spending as a coping mechanism, providing short-term relief while worsening the underlying problem. Recognizing this pattern is the first step to interrupting it. |

"The first step to paying off debt is not a spreadsheet. It is giving yourself permission to look at your finances without judgment, with the same compassion you would offer a friend in the same situation."

SECTION 4

Understanding How Credit Card Interest Really Works

One of the most effective things you can do for your financial situation is deeply understand the mechanism that is working against you. Credit card interest is not complicated, but it is powerful, and its full implications are rarely communicated clearly.

The Mechanics of APR and Compound Interest

APR stands for Annual Percentage Rate, the yearly interest charge expressed as a percentage of your balance. But most credit cards charge interest daily, not annually. Your daily periodic rate is your APR divided by 365. A 24% APR = 0.0658% charged per day.

The balance on which interest is charged is your average daily balance, and if you carry a balance from one month to the next, interest is calculated on both the original balance AND the accumulated interest. This is the compounding effect that makes debt grow so relentlessly.

The Minimum Payment Trap — Illustrated

Scenario | What Actually Happens |

|---|---|

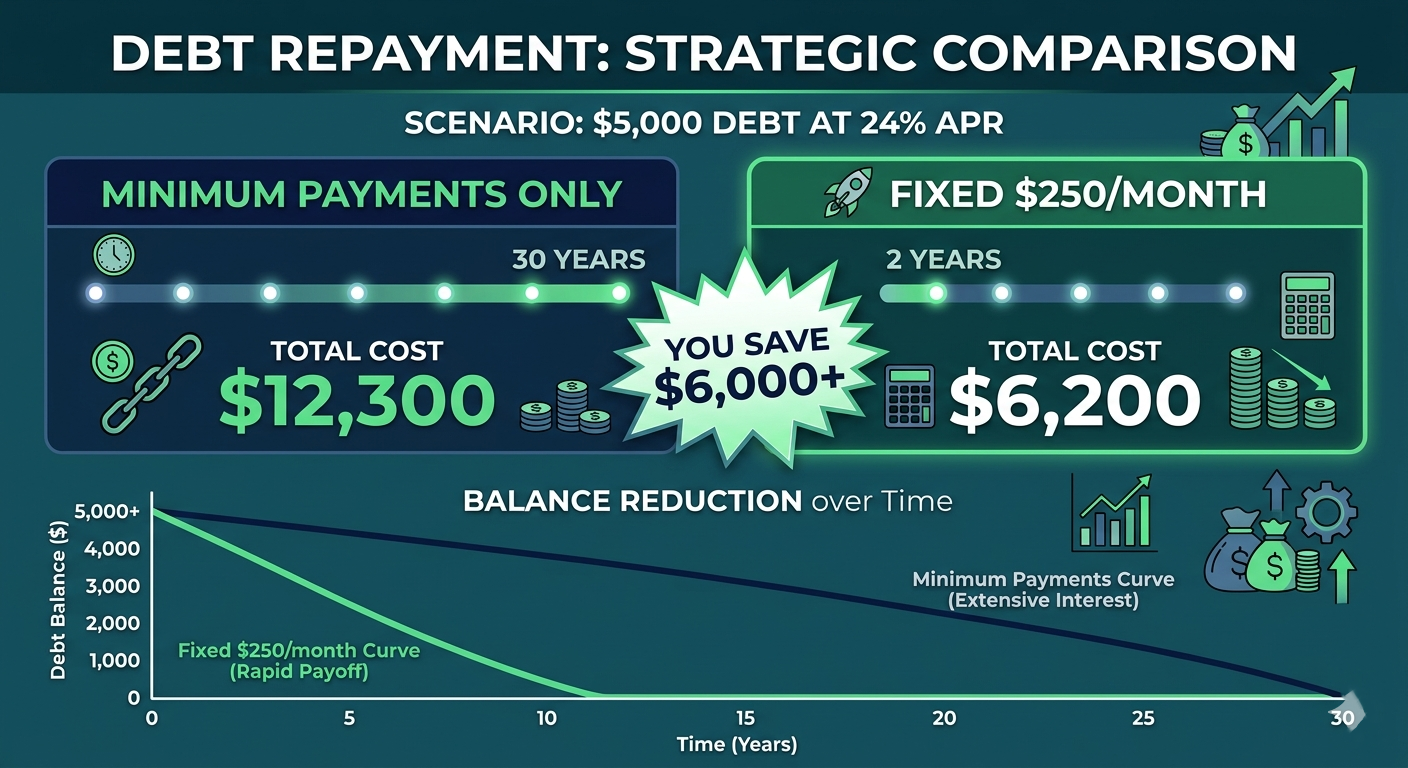

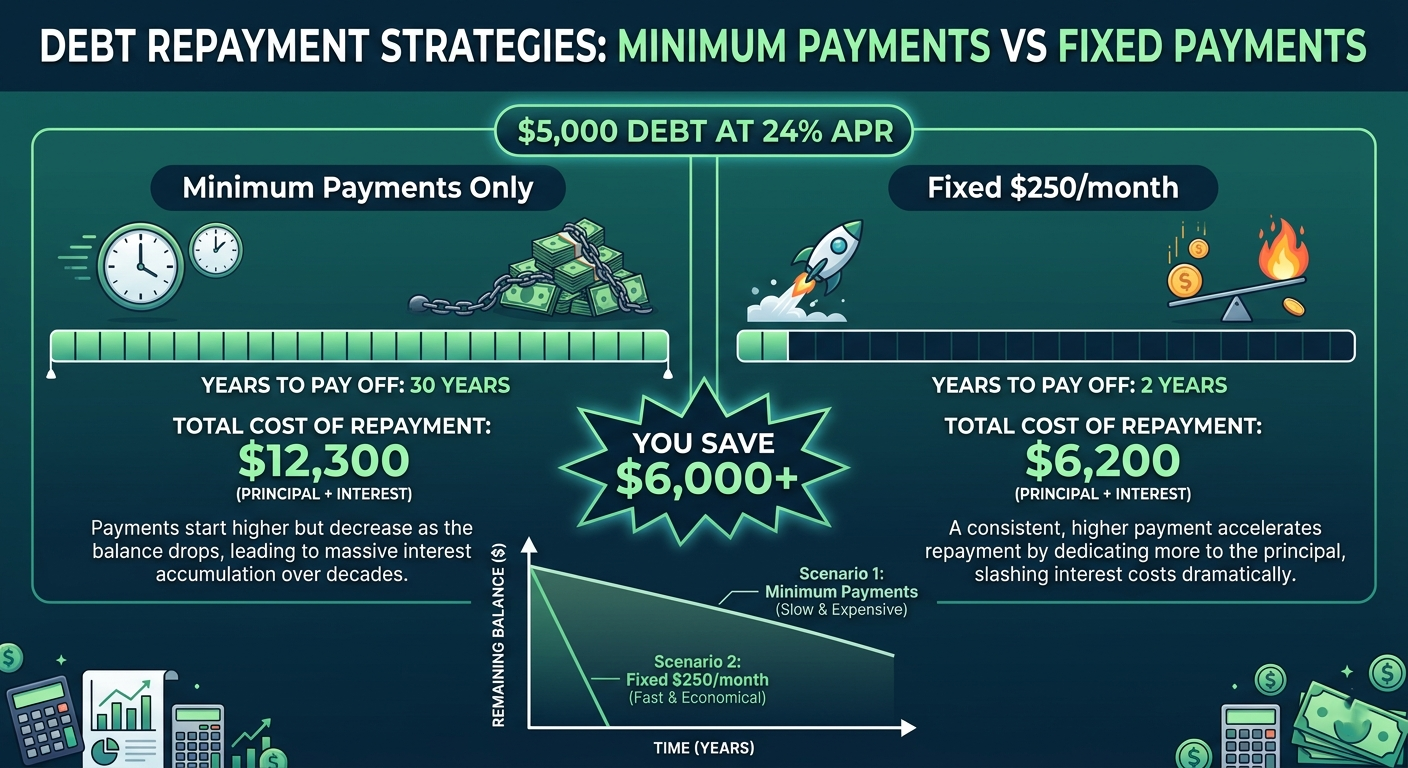

Balance: $5,000 | APR: 24% | Minimum Payment: 2% of balance | Payoff time: Approximately 30 years. Total interest paid: Approximately $7,300. You pay back nearly 2.5x the original balance. |

Balance: $5,000 | APR: 24% | Fixed Payment: $150/month | Payoff time: Approximately 4 years. Total interest paid: Approximately $2,100. You save more than $5,000 compared to minimum payments. |

Balance: $5,000 | APR: 24% | Fixed Payment: $250/month | Payoff time: Approximately 2 years. Total interest paid: Approximately $1,200. More than $6,000 saved compared to minimum payments alone. |

Balance: $5,000 | APR: 24% | Balance Transfer to 0% for 18 months + $280/month | Payoff time: 18 months. Total interest paid: Near zero (balance transfer fee of 3-5% applies). Potential total savings: $7,000+. |

KEY INSIGHT: THE INTEREST-FIRST REALITY |

On a $5,000 balance at 24% APR, you are paying approximately $100 in interest per month. |

A minimum payment of $100-$125 barely covers the interest, meaning virtually nothing comes off your balance. |

This is not a coincidence. Minimum payments are deliberately calculated to maximize the duration of debt. |

Even increasing your minimum payment by $50-$75 per month dramatically accelerates payoff and saves thousands. |

Understanding this mechanism is one of the highest-value financial literacy insights available. |

SECTION 5

The 7 Proven Debt Payoff Strategies

There is no single 'best' debt payoff strategy. The right approach depends on your income, your debt profile, your psychological wiring, and your current financial stability. What matters most is choosing a strategy you can sustain, and starting it. Imperfect action consistently beats perfect inaction.

STRATEGY 1: THE DEBT SNOWBALL METHOD |

The Debt Snowball method, popularized by financial educator Dave Ramsey, involves listing all debts from smallest to largest balance and attacking the smallest balance first, regardless of interest rate. You pay the minimum on all other debts while throwing every available extra dollar at the smallest balance. When it is eliminated, you 'roll' that payment to the next smallest, creating an accelerating 'snowball' of momentum. PROS:✓ Powerful psychological wins, eliminating small debts quickly builds motivation ✓ Simple to implement and easy to track progress ✓ Reduces the number of creditors and payments faster ✓ Research supports its effectiveness due to behavioral momentum (Amar, Ariely et al.) CONS:✗ Not mathematically optimal — you may pay more total interest than the avalanche method ✗ Large high-interest debts grow while you focus on smaller ones ✗ Less effective if the smallest debts have very low balances and the largest have very high rates BEST FOR: People who are feeling emotionally defeated by debt and need early wins to build momentum. Those with multiple small debts cluttering their financial picture. REALISTIC EXPECTATIONS: Most people see their first debt eliminated within 3–6 months, which provides genuine motivational fuel. Expect to pay somewhat more total interest than the avalanche method — the tradeoff is sustainability and momentum. |

STRATEGY 2: THE DEBT AVALANCHE METHOD |

The Debt Avalanche method is the mathematically optimal approach. You list all debts from highest APR to lowest and target the highest-interest debt first, regardless of balance size, paying minimums on all others. This minimizes total interest paid over the life of your debt repayment journey. PROS:✓ Minimizes total interest paid, can save thousands over snowball in high-APR environments ✓ Particularly powerful when the highest-rate debt is also a large balance ✓ Satisfying for analytical thinkers who respond to mathematical optimization CONS:✗ Early wins take longer, high-rate debts are often large balances that take months to eliminate ✗ Can feel demotivating if the first target takes many months to pay off ✗ Requires consistent discipline in the absence of quick psychological wins BEST FOR: Disciplined, analytically oriented people who are motivated by long-term optimization rather than short-term wins. Those with high-APR credit cards as their largest balances. REALISTIC EXPECTATIONS: In a 21%+ APR environment, the avalanche method can save $2,000–$8,000+ over the snowball method depending on debt profile. The cost is slower early psychological rewards. |

STRATEGY 3: BALANCE TRANSFER TO 0% APR |

A balance transfer moves existing high-interest credit card debt to a new card offering a 0% introductory APR period, typically 12 to 21 months. During this period, every payment goes entirely toward reducing principal rather than servicing interest. This can be extraordinarily powerful for accelerating debt elimination if used with discipline. PROS:✓ Every payment reduces balance — no interest leakage ✓ Can save thousands in interest if the balance is cleared within the promotional period ✓ Does not require a debt consolidation loan or changing your spending habits immediately ✓ Several competitive 0% balance transfer offers currently available in 2026 CONS:✗ Requires good-to-excellent credit score (typically 670+) to qualify ✗ Balance transfer fees of 3–5% of transferred amount apply — calculate break-even point ✗ If the balance is not cleared before the promotional period ends, remaining balance reverts to standard APR (often 24%+) ✗ Can encourage continued card spending if spending behavior is not addressed BEST FOR: People with good credit who have a clear, realistic plan to pay off most or all of the transferred balance within the promotional period. Best for balances of $2,000–$15,000. REALISTIC EXPECTATIONS: With a 0% introductory period and disciplined fixed payments, a $7,000 balance transferred and paid at $400/month would be fully eliminated in 17.5 months with near-zero interest cost (compared to $2,000+ at 24% APR). |

STRATEGY 4: DEBT CONSOLIDATION LOAN |

A personal debt consolidation loan replaces multiple high-interest debts with a single loan at a lower interest rate, creating one monthly payment and a defined payoff timeline. In the current rate environment, qualifying borrowers may access personal loan rates of 10–16%, significantly lower than the average 21%+ credit card APR. PROS:✓ Single monthly payment simplifies management ✓ Fixed interest rate and defined payoff timeline creates clarity ✓ Lower interest rate than credit cards means more principal reduction per payment ✓ Loan term gives a concrete end date, psychologically powerful CONS:✗ Requires good credit to access genuinely competitive rates ✗ Origination fees (1–6%) reduce total savings, calculate net benefit carefully ✗ Risk of re-running credit card balances after consolidation if spending habits unchanged ✗ Secured consolidation loans put assets (e.g., home equity) at risk — use with caution BEST FOR: People with multiple high-interest balances across 3+ accounts and good-enough credit to access rates meaningfully lower than their average credit card APR. Those who respond well to simplicity and defined timelines. REALISTIC EXPECTATIONS: A consolidation loan at 13% replacing credit cards averaging 24% on a $12,000 balance saves approximately $4,500–$6,000 in interest over a 4-year repayment term — if no new credit card debt is accumulated. |

STRATEGY 5: NEGOTIATE LOWER INTEREST RATES |

This strategy is dramatically underused, and it costs nothing. Calling your credit card issuer and requesting a lower interest rate is surprisingly effective. Studies show that a significant percentage of cardholders who ask receive a rate reduction. Credit card companies prefer reduced-rate retention to losing a customer to a balance transfer or consolidation. PROS:✓ Zero cost, requires only a phone call ✓ Immediate effect on interest accrual if successful ✓ Can be repeated annually and across all cards ✓ Can be combined with any other strategy ✓ Particularly effective for long-standing customers with consistent payment history CONS:✗ Success is not guaranteed, depends on credit history, payment record, and issuer policy ✗ Rate reduction may be temporary or smaller than desired ✗ Requires proactive communication and potential persistence BEST FOR: Any cardholder, but especially those with a track record of on-time payments, an account open for 2+ years, and a credit score above 650. REALISTIC EXPECTATIONS: Research suggests 50–70% of customers who ask receive some form of rate reduction. A reduction from 24% to 19% on a $5,000 balance saves approximately $250/year in interest — for a 10-minute phone call. |

STRATEGY 6: INCREASE INCOME STRATEGICALLY |

Every dollar of additional income directed entirely toward debt dramatically accelerates your payoff timeline. In the gig and platform economy of 2026, income augmentation options are more accessible than at any previous point, from structured side hustles to monetizing existing skills, time, or assets. PROS:✓ Directly accelerates debt payoff without reducing current spending quality of life ✓ Can be temporary, a focused 6–18 month intensive income push can transform a debt situation ✓ Side income builds skills, confidence, and sometimes long-term earning capacity CONS:✗ Requires available time and energy, which debt stress may have already depleted ✗ Not all income augmentation translates to high enough hourly return to justify the effort ✗ Risk of burnout if sustained at unsustainable pace BEST FOR: People with available time, marketable skills, and the physical or mental energy to add income-generating activity. Particularly powerful when combined with the avalanche or snowball method. REALISTIC EXPECTATIONS: An extra $400–$600/month directed at a $10,000 credit card debt at 22% APR reduces payoff time from 7+ years (minimum payments) to approximately 22–28 months. The mathematics of extra income are extremely favorable. |

STRATEGY 7: BUILD AN EMERGENCY BUFFER WHILE PAYING DEBT |

This strategy addresses one of the most common reasons debt payoff fails: the emergency that sends everything back to credit cards. Building a small starter emergency fund, even $500 to $1,000, while simultaneously paying down debt is a crucial structural protection that many pure debt-payoff frameworks underemphasize. PROS:✓ Prevents re-accumulation of debt from predictable unexpected expenses ✓ Reduces the psychological pressure that makes avoidance more tempting ✓ Creates a positive financial habit that outlasts the debt payoff period ✓ Even $500 covers the majority of common small emergencies that derail debt plans CONS:✗ Redirects some funds from debt payoff in the short term ✗ Interest continues accruing on debt while building the buffer ✗ Requires prioritization discipline, the buffer fund must not be used for non-emergencies BEST FOR: Everyone, but particularly those who have experienced the cycle of paying down cards and then re-charging them due to emergencies. Building even a $500–$1,000 buffer before focusing fully on debt accelerates long-term payoff. REALISTIC EXPECTATIONS: The modest interest cost of building a $1,000 emergency fund before aggressively paying debt is typically $15–$25/month, a very small price for the structural protection it provides against re-accumulating the debt you are working to eliminate. |

SECTION 6

The 2026 Debt Survival Budget Framework

A budget is not a punishment. It is a map. When you are in debt, a well-constructed budget is the single most important tool you have, because it reveals where your money is actually going versus where you want it to go, and creates the cash flow you need to accelerate your payoff.

The Bare-Bones Expense Triage

Before building a budget, conduct an honest triage of your expenses. Categorize every regular outgoing cost into one of three buckets:

Non-negotiable essentials: Housing, utilities (basic), food, minimum debt payments, healthcare, and transportation to work. These must be paid.

Reducible essentials: Groceries (can optimize), transportation (can reduce), insurance (can shop), phone (can downgrade plan).

Discretionary or eliminable: Streaming services, subscriptions, dining out, entertainment, impulse purchases. Everything in this category is a candidate for temporary reduction.

The 2026 Debt Payoff Budget Template

Budget Category | Recommended Allocation / Target % |

|---|---|

| Housing (rent or mortgage) | No more than 30% of take-home income. If above this, explore reduction options. |

| Food (groceries + essential dining) | 10–12% — meal planning and grocery optimization are high-leverage here |

| Transportation | 10–15% — includes fuel, insurance, public transit, maintenance |

| Healthcare & Insurance | 5–8% — non-negotiable but can sometimes be optimized |

| Utilities (basic: electric, gas, water) | 3–5% — review usage patterns and switch to budget billing |

| Minimum Debt Payments | Mandatory — list every minimum separately and ensure they are always paid |

| EXTRA DEBT PAYOFF (avalanche/snowball target) | Target 10–20%+ of take-home — this is your wealth-building engine during debt payoff |

| Starter Emergency Fund Contribution | 1–3% until $500–$1,000 is reached, then redirect to debt payoff |

| Phone, Internet (basic) | 2–4% — consider downgrading plans during debt payoff sprint |

| Subscriptions / Entertainment | 0–3% — perform a subscription audit; cancel unused or duplicative services |

| Personal care and clothing (essentials) | 2–3% — temporary reduction, not elimination |

| Everything else | Whatever remains after the above — track carefully |

Subscription Audit: High-Leverage, Low-Effort

The average household pays for 4–7 subscription services they do not actively use. A subscription audit, going through every recurring charge on your bank and credit card statements, takes 30 minutes and regularly surfaces $40–$120/month in recoverable cash flow. Direct every dollar found directly to your target debt.

SECTION 7

Debt Consolidation: Helpful Tool or Dangerous Trap?

'Debt consolidation' is one of the most searched personal finance terms in 2026, and for good reason. The concept is genuinely powerful. But the landscape includes both legitimate, helpful financial products and predatory services that exploit financially vulnerable people. Knowing the difference is essential.

Legitimate Debt Consolidation Options

Option | How It Works / When It Helps / Risks |

Personal Consolidation Loan (from a bank, credit union, or reputable online lender) | Replaces multiple debts with a single loan at (ideally) a lower APR and fixed payment term. Requires good credit for competitive rates. Best from established financial institutions or credit unions. Avoid lenders charging origination fees above 6%. Verify APR in writing before accepting. |

Balance Transfer Credit Card (0% intro APR) | Transfers balances to a new card with a 0% promotional period. Requires good-to-excellent credit. Carry a clear payoff plan for the intro period. Calculate the break-even on the transfer fee (typically 3–5%). Best for balances you can realistically clear within the promo window. |

Home Equity Loan / HELOC | Uses home equity as collateral for a lower-rate loan to pay off higher-rate debt. Dramatically lower interest rates possible (6–10%). CRITICAL WARNING: Your home is the collateral. Missing payments creates foreclosure risk. Only appropriate for financially disciplined homeowners with significant equity and stable income. |

Credit Union Loans | Many credit unions offer personal loans at significantly better rates than banks or online lenders — particularly for members with fair (not just excellent) credit. If you belong to a credit union, explore their debt consolidation loan options first. |

Non-Profit Credit Counseling / Debt Management Plans (DMP) | A non-profit credit counseling agency negotiates with creditors to reduce interest rates and consolidates payments into one monthly payment to the agency. Fees are typically $25–$50/month. Takes 3–5 years. Requires closing credit accounts. NFCC (National Foundation for Credit Counseling) member agencies are a trustworthy starting point. |

WARNING: PREDATORY DEBT RELIEF SERVICES TO AVOIDDEBT SETTLEMENT COMPANIES:For-profit companies that collect fees while you stop paying creditors, promising to negotiate lump-sum settlements. Your credit is destroyed, creditors can still sue, fees are high, and results are not guaranteed. Approach with extreme caution. ADVANCE FEE LOAN SCAMS:Legitimate lenders do not charge upfront fees before providing a loan. Any 'lender' requiring payment before disbursing funds is almost certainly a scam. CREDIT REPAIR COMPANIES:No company can legally remove accurate information from your credit report. Anyone promising to 'clean' or 'fix' your credit for a fee is likely misleading you. You can dispute errors for free directly with the credit bureaus. VERY HIGH-FEE CONSOLIDATION LOANS:Some online lenders targeting poor-credit borrowers charge origination fees of 8–12% and APRs of 30–36%. These are not solutions, they are repackaged debt traps. VERIFY:Check any financial service with the Consumer Financial Protection Bureau (CFPB) complaint database and your state attorney general's office before engaging. |

SECTION 8

How to Survive Financially Right Now

Sometimes the priority is not the optimal long-term strategy, it is getting through this month without falling further behind. The following tactics are for people under acute financial pressure who need immediate, practical relief.

Immediate Stabilization Tactics

Call your creditors before missing payments, not after. Most major credit card issuers have hardship programs, temporarily reduced interest rates, waived fees, or reduced minimum payments, for customers experiencing financial difficulty. These programs are rarely advertised but widely available. One call can change your minimum payment situation for 3–12 months.

Negotiate utility bills and recurring services. Internet providers, phone carriers, and some utilities have retention programs and hardship rates available to customers who ask. Call each provider, explain your situation, and ask specifically for their hardship or retention discount.

Grocery cost optimization without sacrifice. Switching to a combination of store brands (which are often manufactured by the same companies as premium brands), strategic use of loss-leader sales, and meal planning around what is already in the pantry can reduce a typical family grocery bill by $100–$200/month without meaningful quality reduction.

Identify community resources. Food banks, community assistance programs, LIHEAP (Low Income Home Energy Assistance Program), and local non-profit financial assistance are available in most communities, and using them is not failure. It is strategic resource management that frees cash flow for debt repayment.

Sell before you borrow. Before taking on new debt for a non-emergency, consider whether anything in your possession, unused items, electronics, furniture, clothing, could be sold on marketplace apps to fund the need.

Pause retirement contributions temporarily and deliberately. This is controversial advice, but redirecting the employer match minimum is always wise. Temporarily pausing contributions above the employer match during a debt payoff sprint can free $200–$500/month. This is a time-limited, strategic trade-off, not a permanent change. Resume contributions as soon as high-interest debt is eliminated.

Explore income-based repayment options for federal student loans. If student loans are part of your debt burden, federal income-driven repayment (IDR) plans cap payments as a percentage of discretionary income and can free significant monthly cash flow for credit card debt elimination.

SECTION 9

Common Debt Mistakes People Make

Common Mistake | Why It Worsens the Situation, and What to Do Instead |

Avoiding statements and account monitoring | Financial avoidance allows debt to compound in silence and prevents the informed decision-making needed to address it. Looking at your balances regularly, however uncomfortable, is a prerequisite for control. |

Paying minimums and considering the problem managed | Minimum payments are designed to maximize the duration of debt. They are not a debt strategy, they are a debt maintenance strategy. Always pay more than the minimum, even by $20–$50. |

Taking on new high-interest debt to pay old high-interest debt | This is financial treadmill behavior. Payday loans, cash advances, and new high-APR cards taken to service existing debt typically worsen the situation. Verify any new credit product has a materially lower APR before proceeding. |

Using retirement savings to eliminate debt | Withdrawing from a 401(k) before age 59½ triggers income tax plus a 10% penalty, effectively costing 30–40% of the withdrawn amount immediately. A 24% APR on credit card debt is expensive; a 35%+ effective withdrawal penalty is usually far worse. |

Falling for predatory debt settlement or 'credit repair' services | As described in Section 7, these services frequently charge high fees while delivering minimal legitimate benefit and sometimes worsening the credit and legal situation. |

Budgeting without accounting for irregular expenses | Budgets that cover monthly recurring costs but forget annual or irregular expenses (car registration, holiday spending, medical bills) are set up to fail. Build an 'irregular expense' category and divide annual costs by 12. |

Stopping debt payoff after early progress | The first $1,000–$2,000 of debt payoff progress is motivationally the hardest and the easiest to abandon. Those who push through the early phase build momentum that makes the rest dramatically easier. |

Not communicating with a partner about finances | Shared debt in a relationship that does not involve shared financial transparency and shared strategy will almost always fail. One partner's progress is undermined by the other's spending if there is no joint framework. |

SECTION 10

Realistic Debt Recovery Stories

The following composite scenarios reflect the kinds of debt situations and recoveries that occur in real households. Names and specific details are illustrative. The strategies and outcomes reflect what is genuinely achievable with sustained, realistic effort.

Marcus, 34 — The Young Professional Who Got Ahead of Minimum PaymentsMarcus had $11,400 spread across four credit cards. all carrying APRs between 21% and 26.9%. He was paying minimum payments on each and had been 'managing' his debt this way for three years without making meaningful progress. His minimum payments totaled $248/month; the interest accumulating each month was approximately $205. He was paying nearly $250 to reduce his balance by $43. After running an honest budget analysis, Marcus found $320/month of genuinely recoverable cash flow, subscription cancellations ($67/month), a phone plan downgrade ($45/month), and a conscious reduction in food delivery spending ($208/month). He applied the avalanche method: paying minimums on three cards while attacking the 26.9% card with everything available. Within 14 months, his first two cards were eliminated. By month 28, he was debt-free. Total interest paid: approximately $4,200. Total interest he would have paid at minimum-only payments: approximately $17,400. His savings: more than $13,000, and 25+ fewer years of payments. |

The Reyes Family — Surviving Inflation Through Budget SurgeryMaria and Carlos Reyes, both 41, had accumulated $22,000 in credit card debt over three years, not through reckless spending, but through a combination of inflation-driven grocery and utility cost increases, a medical bill that exceeded their insurance coverage, and two car repairs. Their combined income was $88,000. They felt simultaneously middle-class and financially underwater. A credit counselor helped them identify $680/month in recoverable expenses through a detailed cash flow audit: an unused gym membership ($95), three overlapping streaming services ($47), a grocery bill that dropped $240/month through meal planning and store-brand switching, and a refinanced car insurance policy saving $298/month. They enrolled in a Debt Management Plan through an NFCC-accredited agency, which negotiated their average APR from 22.4% to 7.8% and consolidated all payments. Three and a half years later, they are debt-free. Their credit scores have improved significantly. They now direct the former DMP payment into their emergency fund. |

Jasmine, 29 — Using a Balance Transfer to Eliminate $8,500 in 16 MonthsJasmine had $8,500 on a single credit card at 24.9% APR. She qualified for a 0% balance transfer card with an 18-month introductory period and a 3% transfer fee. After paying the $255 transfer fee, she had 18 months to pay off $8,755 interest-free. She calculated she needed to pay $486/month, which was within reach if she took on an additional 6 hours per week of freelance work through an online platform. She paid the balance off in 16 months, with two months to spare. Total interest paid: $255 (the transfer fee). Compared to staying on her original card at minimum payments, she saved approximately $8,400 in interest over the equivalent time period. 'The math was almost too obvious once I saw it,' she said. 'The hardest part was believing I would actually qualify for the card.' |

Devon, 38 — A Gig Worker Rebuilding After OverspendingDevon worked as a freelance video editor. Income variability was his norm, good months were great, slow months were dangerous. Over two years, slow months had built $14,200 in credit card debt across five cards. His income averaged $5,800/month but ranged from $3,200 to $8,500. Standard fixed budgeting wasn't working because his expenses were variable too. His financial coach helped him build a percentage-based budget: every time he received income, he allocated percentages immediately rather than fixed dollar amounts, 40% for needs, 20% for debt payoff, 10% for emergency fund, 10% for taxes, 20% for everything else. This meant debt payments scaled with income automatically. In high-earning months, his debt payment was $1,700; in slow months, $640. His emergency fund grew to $3,000. Within 26 months, all five cards were paid off. The variability-adjusted system was the key. |

SECTION 11

When to Seek Professional Financial Help

There are situations where individual effort and strategy are not enough, where the complexity, severity, or emotional weight of a debt situation requires professional support. Recognizing when to seek help is a sign of financial intelligence, not weakness.

Situation / Trigger | Who Can Help and What They Offer |

Debt payments consistently exceeding 40-50% of take-home income despite budget efforts | Non-profit credit counseling agency (NFCC member): Debt Management Plan, creditor negotiation, lower interest rates, consolidated payments over 3–5 years. |

Creditors threatening lawsuits or wage garnishment | Consumer bankruptcy attorney (many offer free initial consultations): Assess whether Chapter 7 or Chapter 13 bankruptcy provides a legal path to reset. Bankruptcy is a legal tool, not a moral failing, and for some situations, it is the most appropriate financial decision. |

Debt collectors harassing in violation of the FDCPA | Consumer Financial Protection Bureau (CFPB) complaint portal; State attorney general's office; Consumer rights attorney. Know your rights: the Fair Debt Collection Practices Act (FDCPA) restricts what collectors can legally do. |

Financial stress severely impacting mental health | Financial therapist or financial coach (not planner — no license required) who combines financial education with psychological support for money-related anxiety, shame, and avoidance. |

Complex debt situation with mixed student loans, credit cards, medical debt, and possible bankruptcy | Fee-only, fiduciary Certified Financial Planner (CFP) who specializes in debt resolution, charges hourly or flat fee, not commission. Find via NAPFA.org or Garrett Planning Network. |

Identity theft or unauthorized accounts | Federal Trade Commission (FTC) at IdentityTheft.gov; credit bureau fraud departments; Consumer protection attorney if damages are significant. |

SECTION 12

The Role of Emergency Funds in Debt Recovery

The most common reason debt payoff plans fail is not a lack of discipline. It is the car that breaks down in month four. The medical bill in month seven. The appliance that dies in month twelve. Without a financial buffer, every one of these predictable emergencies sends the budget back to the credit card — re-accumulating the debt that was so laboriously paid down.

The Starter Emergency Fund Framework

BUILDING YOUR $1,000 EMERGENCY BUFFER |

STEP 1:Open a separate savings account, ideally a high-yield savings account (HYSAs in 2026 offer 4.5–5.2% APY). Name it 'Emergency Buffer Only.' |

STEP 2:Set a recurring automatic transfer of $25–$50/week from your checking account to the emergency buffer. Automate this so it requires no willpower. |

STEP 3:Direct any unexpected income windfalls (tax refunds, overtime, bonuses, side income) to the emergency buffer first until the target balance is reached. |

STEP 4:Establish what constitutes a legitimate emergency: car repairs, medical costs, genuine appliance failures, job loss. 'Emergency' does not include sales, events, or lifestyle expenses. |

STEP 5:Once the starter buffer is reached ($500–$1,000), redirect all additional capacity to your debt payoff target (avalanche or snowball). |

STEP 6:After all high-interest debt is eliminated, build toward a 3–6 month full emergency fund. |

SECTION 13

Debt Payoff Calculator Section

Understanding your specific numbers, your actual payoff timeline, your total interest cost, and the impact of different monthly payment amounts, is one of the highest-value activities in debt recovery. Numbers make the abstract concrete. They turn 'I should pay more' into 'if I add $150/month, I'm debt-free in 23 months instead of 9 years.'

Manual Calculation Examples

Balance | APR | Monthly Payment | Months to Pay Off / Total Interest |

| $5,000 | 24% | $105 (minimum, ~2%) | ~28 years / ~$12,800 total interest |

| $5,000 | 24% | $200/month (fixed) | ~32 months / ~$1,400 total interest |

| $5,000 | 24% | $350/month (fixed) | ~16 months / ~$960 total interest |

| $5,000 | 0% (transfer, 18 mo.) | $280/month (to clear in 18 mo.) | 18 months / ~$150 (transfer fee only) |

| $12,000 | 22% | $240 (minimum) | ~25+ years / $24,000+ total interest |

| $12,000 | 22% | $450/month (fixed) | ~37 months / ~$4,200 total interest |

| $12,000 | 13% (consolidation) | $350/month (fixed) | ~42 months / ~$2,500 total interest |

Where to Access a Debt Payoff Calculator

Undebt.it (free, includes snowball and avalanche visual planners)

NerdWallet Debt Payoff Calculator (free, includes side-by-side method comparison)

Bankrate Debt Payoff Calculator (free, allows custom payment scenarios)

Consumer Financial Protection Bureau (CFPB) financial tools (free government resource)

SECTION 14

The Future of Consumer Debt in the AI Economy

Development | What It Means for Consumers in 2026 and Beyond |

| AI-Driven Budgeting and Financial Coaching | AI-powered personal finance apps are moving beyond simple expense categorization toward proactive cash flow coaching, alerting users to upcoming financial risks, suggesting payment optimizations, and modeling payoff scenarios in real time. Apps like Monarch Money, YNAB, and newer AI-native entrants are making sophisticated financial analysis accessible to anyone with a smartphone. |

| Automated Debt Payoff Tools | Several banking apps and fintech platforms now offer 'round-up' debt payoff features, automatically applying small additional amounts to target debts. While individually modest, these automated micro-payments add up and require zero willpower to maintain. |

| Evolution of Credit Scoring | Traditional FICO scores are increasingly complemented by alternative credit data, including rent payment history, utility payments, and banking behavior, expanding access to better-rate credit products for those with thin credit files but strong financial behavior. |

| BNPL Debt Visibility | Regulatory pressure and credit bureau policy changes are bringing Buy Now Pay Later debt into standard credit reporting in 2026, increasing both visibility and accountability for this rapidly growing debt category. |

| Financial Literacy as Infrastructure | Growing recognition of financial literacy gaps is driving public and private investment in financial education, at the employer level (financial wellness benefits), the school level, and through digital content platforms reaching younger consumers earlier in their financial lives. |

| Interest Rate Trajectory | While no forecast is certain, the Federal Reserve's rate environment in 2026 remains elevated relative to the 2010–2020 decade. Credit card APR relief is not imminent, making the strategies in this guide as relevant as ever. |

SECTION 15

Conclusion: One Payment at a Time

Debt at the scale many households are carrying in 2026 is not a personal moral failure. It is the predictable outcome of a financial environment designed to keep people in debt, high interest rates, minimum payment structures, easy credit access, wage erosion, and a cultural silence around financial struggle that prevents people from getting help until the situation has become acute.

The path out is not dramatic. It is consistent. It is choosing one strategy, snowball, avalanche, balance transfer, negotiation, and executing it imperfectly but persistently. It is finding $50 in a budget audit and directing it at the target card instead of absorbing it elsewhere. It is making the phone call to ask for a lower rate. It is building $500 in an emergency buffer so that one car repair does not undo three months of progress.

Every dollar of debt you eliminate eliminates interest that would have compounded against you for years. Every month you sustain your plan is a month closer to the financial breathing room that transforms daily life, less anxiety, better sleep, stronger relationships, more choices. That is what you are working toward.

|

YOUR NEXT THREE STEPS |

STEP 1 THIS WEEK:List every debt, balance, APR, minimum payment. Calculate your total debt and average interest rate. Know your actual numbers. |

STEP 2 THIS WEEK:Run a subscription and expense audit. Find at least $50–$100/month in recoverable cash flow. Direct it to your highest-interest or smallest balance. |

STEP 3 THIS MONTH:Choose your primary strategy (snowball, avalanche, or balance transfer if eligible). Write it down. Set a calendar reminder to review progress every 30 days. |

|

FAQ

Frequently Asked Questions

Q: What is the fastest way to pay off credit card debt?

A: The fastest pure-interest-elimination method is the Debt Avalanche, targeting the highest APR card first. The fastest method that maximizes motivation and reduces number of accounts is the Debt Snowball. If you qualify for a 0% balance transfer with a clear plan to pay off the balance within the promotional period, a well-executed balance transfer can be even faster in real terms. The 'fastest' method is ultimately the one you sustain consistently, pick the approach that fits your psychology and income, and execute it with discipline.

Q: How much does it actually cost to pay only the minimum payment?

A: On a $5,000 balance at 24% APR, paying only the minimum payment (approximately $100/month declining) results in a payoff time of approximately 28–30 years and total interest paid of approximately $12,000–$13,000, nearly triple the original balance. Increasing your payment to $300/month at the same APR reduces payoff to approximately 20 months and total interest to approximately $1,000. The minimum payment is not debt management, it is debt preservation at maximum cost.

Q: Will debt consolidation hurt my credit score?

A: In the short term, applying for a consolidation loan or balance transfer card creates a hard inquiry that may temporarily reduce your credit score by 3–5 points. Over the medium to longer term, debt consolidation typically improves credit scores, because consistent on-time payments build positive history, credit utilization decreases as balances fall, and reducing the number of delinquent or high-utilization accounts has a net positive effect. The temporary short-term dip is almost always worth the medium-term benefit.

Q: Should I stop contributing to my 401(k) to pay off debt?

A: This depends on your specific situation. A general framework: always contribute at least enough to capture your employer's full match, that is an immediate 50–100% return on your investment, which almost no debt reduction strategy can match. Beyond the match: if your credit card APRs are above 10–12%, many financial planners suggest temporarily pausing contributions above the employer match to direct funds toward high-interest debt elimination. Withdraw from retirement accounts early only as an absolute last resort, the 10% penalty plus income tax typically makes this among the most expensive 'solutions' available.

Q: What if I can't afford even the minimum payments?

A: Contact your creditors immediately, before missing payments. Most major issuers have hardship programs that temporarily reduce minimum payments or interest rates for customers experiencing financial difficulty. These programs are real and available, but you have to ask for them. If you are already missing payments and facing collection activity, contact an NFCC-accredited non-profit credit counseling agency, they can help negotiate on your behalf and assess all available options including Debt Management Plans. If your debt is truly unmanageable relative to your income and assets, a consultation with a consumer bankruptcy attorney (many offer free consultations) is appropriate to understand your full legal options.

Q: Is it better to pay off debt or save an emergency fund first?

A: The standard financial planning answer in 2026: build a $500–$1,000 starter emergency fund first, then focus intensively on high-interest debt elimination. The reasoning is structural: without any cash buffer, the first unexpected expense goes on the credit card, re-accumulating the debt you just paid. A small emergency fund prevents this cycle. Once high-interest debt is eliminated, build toward a 3–6 month full emergency fund before aggressively investing.

Q: Can I negotiate my credit card interest rate myself?

A: Yes! and many people do, successfully. Call the number on the back of your card and explain that you have been a loyal customer, you have (hopefully) maintained on-time payments, and you are seeking a lower interest rate. Ask specifically for a rate reduction, not a hardship program, not a payment plan. Studies suggest 50–70% of customers who ask receive some reduction. The worst outcome is a 'no.' Call back in 3–6 months and ask again. If you have improved your credit score since you last asked, mention it.

Trusted Financial Wellness Resources

Organisation / Resource | What They Offer |

| National Foundation for Credit Counseling — NFCC (nfcc.org) | Directory of non-profit credit counseling agencies; Debt Management Plan information; free budgeting resources. |

| Consumer Financial Protection Bureau (consumerfinance.gov) | Free financial tools, complaint database, credit card comparison, debt collection rights information. |

| Federal Trade Commission — Consumer Advice (consumer.ftc.gov) | Debt relief scam identification, credit reports and scores, consumer rights guides. |

| IdentityTheft.gov (identitytheft.gov) | FTC resource for identity theft recovery, unauthorized account disputes, step-by-step resolution plans. |

| NAPFA — National Association of Personal Financial Advisors (napfa.org) | Directory of fee-only, fiduciary financial planners. Best for complex debt situations requiring certified professional guidance. |

| Undebt.it (undebt.it) | Free debt payoff calculator and planner with snowball, avalanche, and custom strategy visualization. |

| AnnualCreditReport.com | Free annual credit reports from all three major bureaus (Equifax, Experian, TransUnion) — legally mandated and no subscription required. |

| Benefits.gov (benefits.gov) | Federal government portal for identifying assistance programs you may qualify for — LIHEAP, SNAP, Medicaid, and others. |

IMPORTANT DISCLAIMER: This article is intended for educational and informational purposes only. It does not constitute professional financial, legal, or tax advice. Every financial situation is unique. Before making significant financial decisions, including debt consolidation, bankruptcy, or investment changes, consult a qualified financial advisor, attorney, or credit counselor. The author and publisher are not responsible for financial outcomes resulting from application of information in this article. All interest rate and balance figures used in examples are illustrative; actual rates and terms vary by lender and individual creditworthiness.